Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If you’ve seen headlines about home prices dropping, it’s easy to wonder what that means for the value of your home, too. Here’s what you really need to know.

Even with slight price declines in some markets, data shows you’re likely still way ahead. And that’s thanks to your home equity.

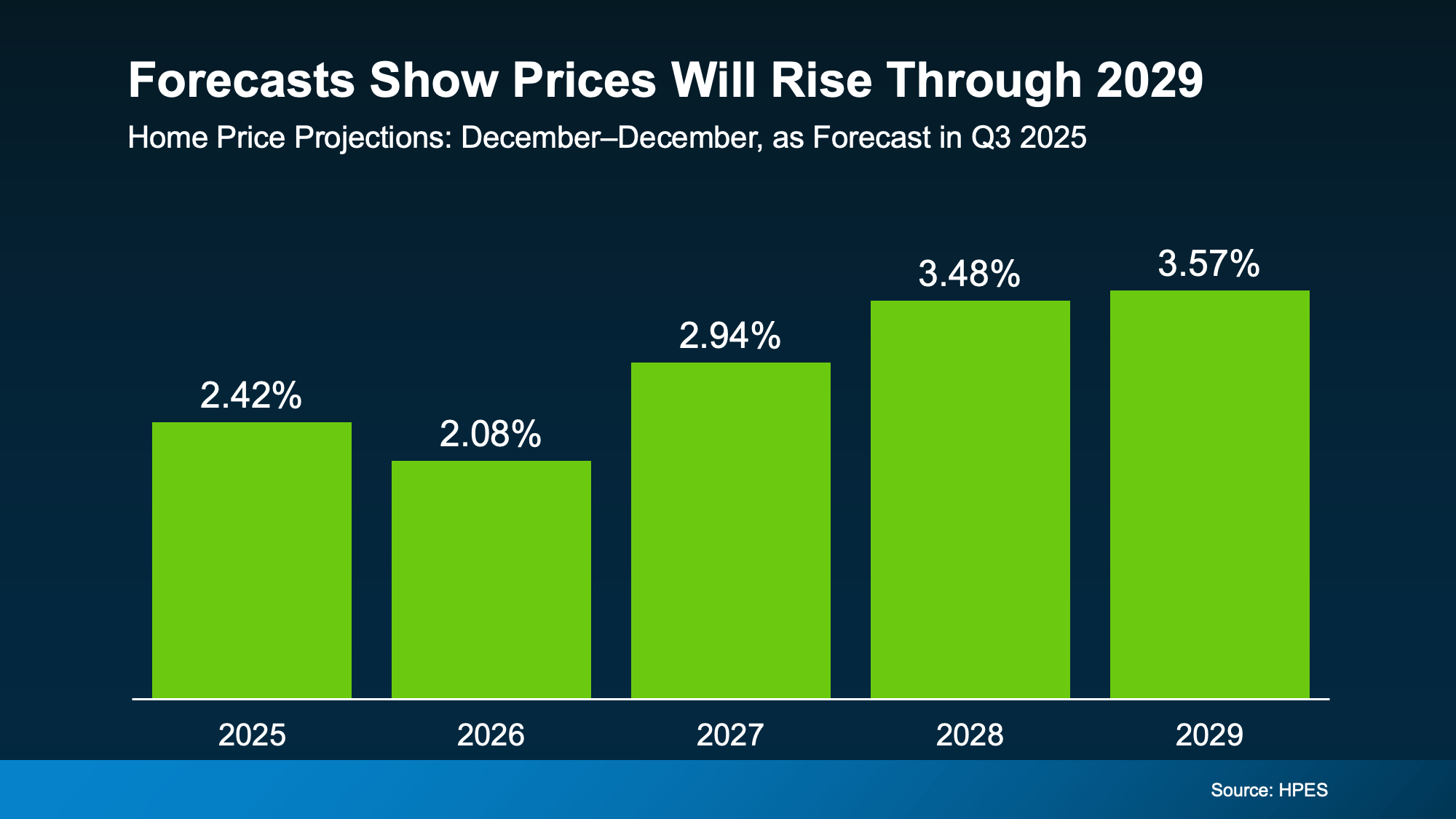

The Relationship Between Home Prices and Equity

Home equity tends to move in sync with home prices. When prices rise, equity builds. When prices cool (even just slightly), equity growth does too. Here’s how that’s played out lately.

After the record-setting home price surge of 2020 and 2021, a slight cooling was inevitable.

At the time, the number of homes for sale reached a record low. That caused home values (and your equity) to increase significantly as buyers competed for limited inventory.

But prices couldn’t continue to rise at that intense pace forever. The market had to moderate at some point, and that’s exactly what we’re seeing right now.

As more homes have come on the market this year, price growth slowed – so, equity gains did too. And that doesn’t mean you’ve lost ground.

Putting it into Perspective

You probably still have far more equity than you did just a few years ago. And that puts you in a strong position if you want to sell. Here’s the data to prove it.

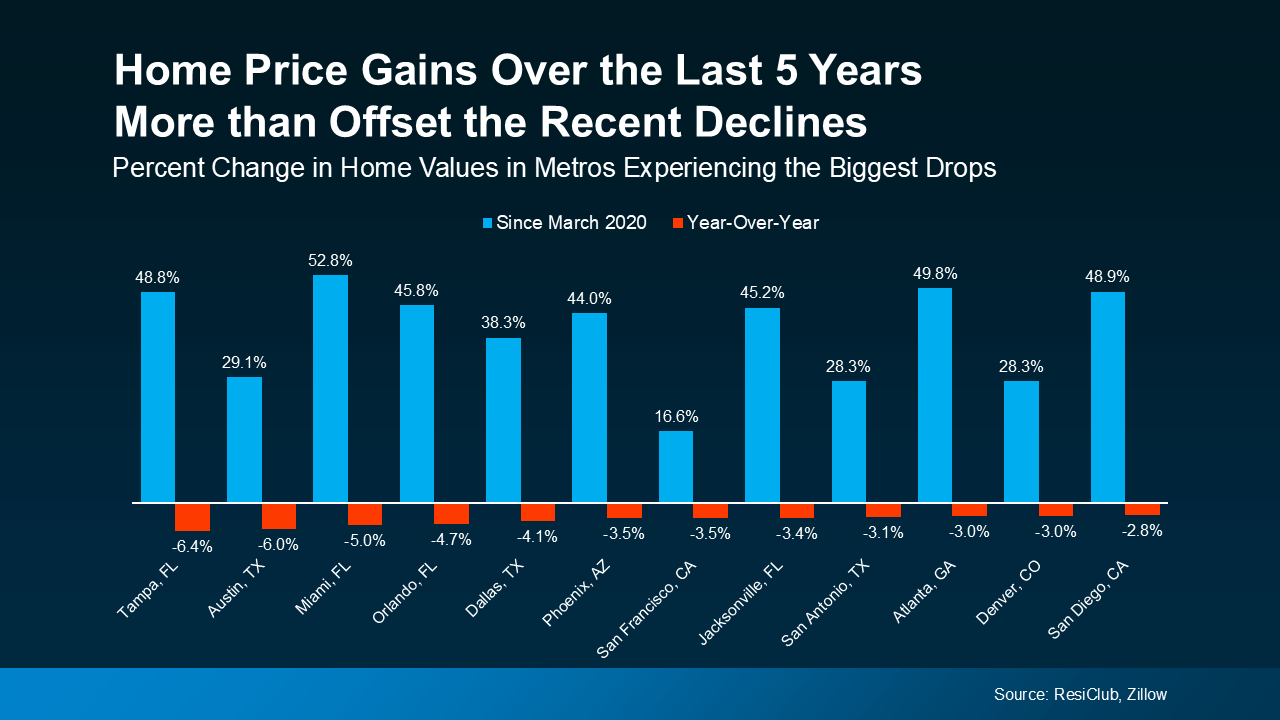

According to research from Zillow, home prices have risen a staggering 45% nationwide since March of 2020. That’s a big jump.

In the majority of markets, prices are still rising, albeit at a much slower pace. However, even in the metros where prices are experiencing the most significant declines (those making the headlines), the average drop is only about 4%.

So, what’s that really mean? In most places, prices are on the rise, so this isn’t even a concern. However, in the few metros where prices are cooling off slightly, the 5-year gains more than offset those small dips.

In other words, these modest declines can’t erase years of growth. Homeowners who’ve been in their houses for several years are still way ahead. Big time. And that’s true pretty much everywhere.

In other words, these modest declines can’t erase years of growth. Homeowners who’ve been in their houses for several years are still way ahead. Big time. And that’s true pretty much everywhere.

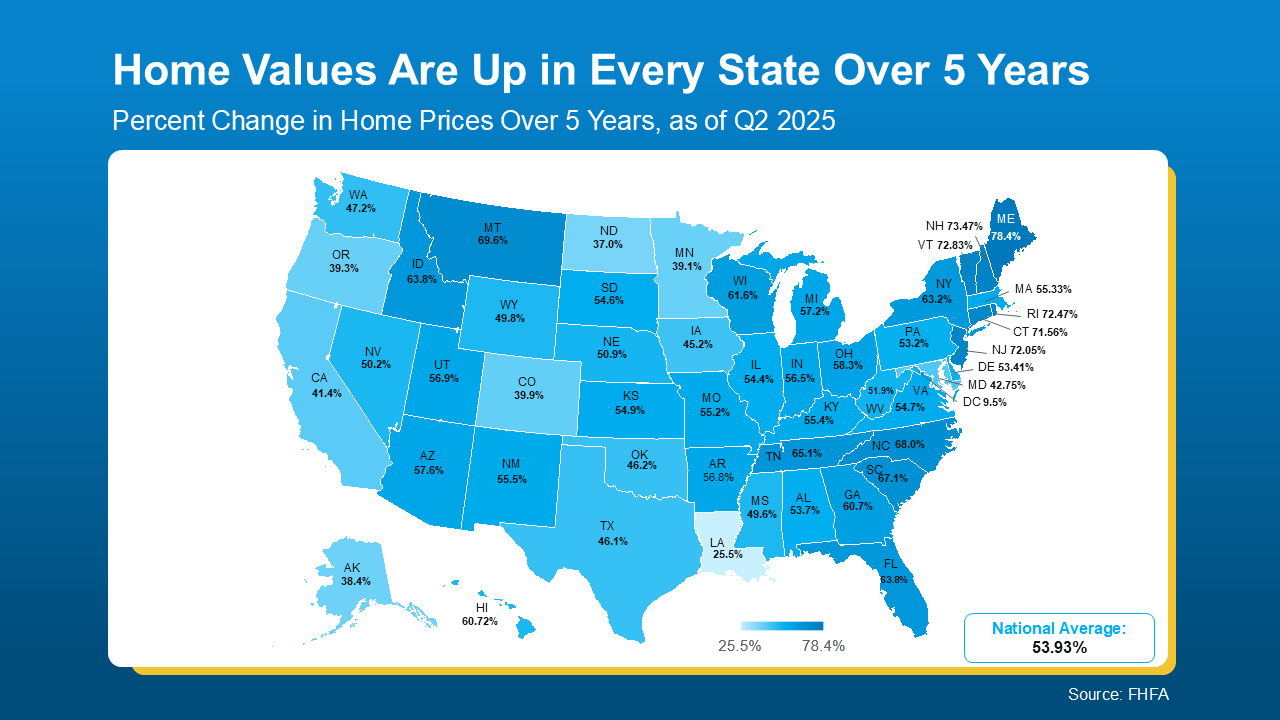

Data from the Federal Housing Finance Agency (FHFA) helps paint this picture. Let’s cast a slightly wider net and look at a state-by-state level this time. Every single state has seen prices increase over the last five years. And that means homeowners in each state have much more equity than they did just 5 years ago (see graph below):

Odds are, in most places, if you’ve owned your home for more than a few years, you’ve already built the kind of equity many people could only dream about before the pandemic. And if you sell, you can use the proceeds to help you downsize or move up.

Odds are, in most places, if you’ve owned your home for more than a few years, you’ve already built the kind of equity many people could only dream about before the pandemic. And if you sell, you can use the proceeds to help you downsize or move up.

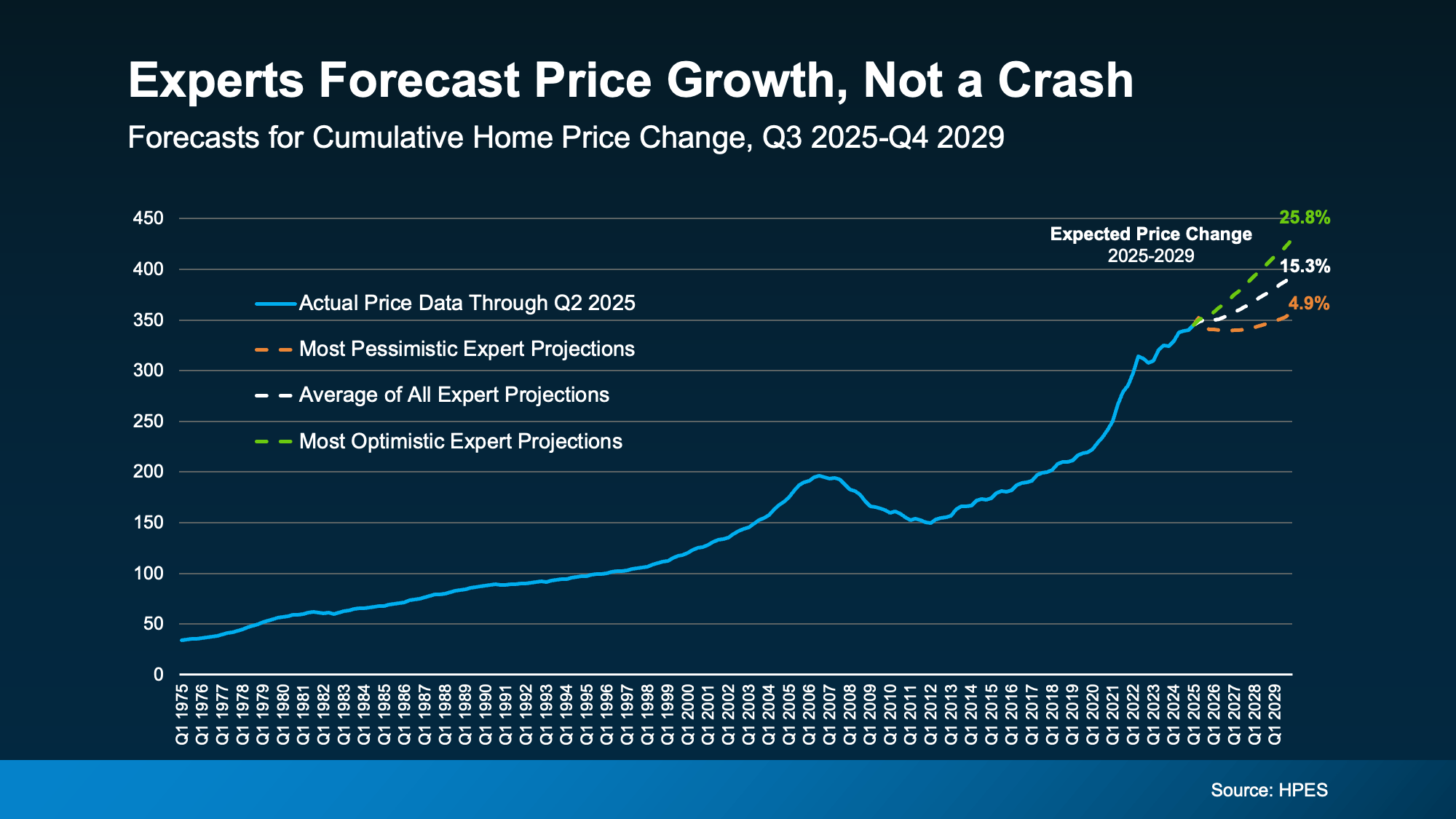

And just in case you’re worried prices will crash and your equity will take a bigger hit in the near future, here’s what Jake Krimmel, Senior Economist at Realtor.com, has to say:

“The slight recent declines in aggregate value and total home equity are not cause for concern . . . Although the market is coming into better balance, large price declines nationally are extremely unlikely in the near term . . .”

The price moderation we’ve seen lately isn’t a cause for concern. It’s a signal of a market that’s finding its balance again after several years of unsustainable price growth. After several years of significant price appreciation, most homeowners remain in a powerful position.

Bottom Line

Even with prices coming down in some markets, today’s homeowners are still sitting on near record amounts of equity.

If you’re wondering how much equity you have (or how far ahead you really are), let’s connect.

You might be surprised by what your home is actually worth today.

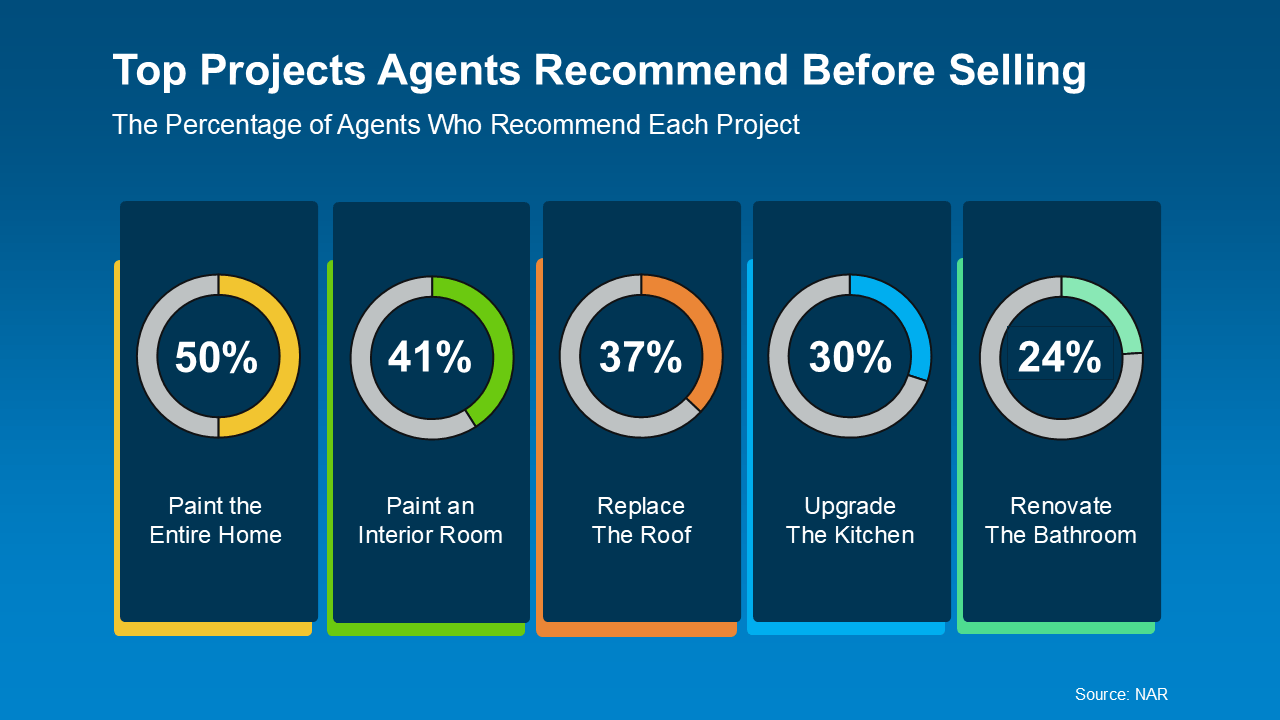

Just remember, what’s worth updating really depends on the homes you’re competing with in your market. Some areas don’t have a ton of inventory, so little updates may be all you need to tackle. In other areas, there are far more homes for sale, so you may need to do a bit more to make your house stand out.

Just remember, what’s worth updating really depends on the homes you’re competing with in your market. Some areas don’t have a ton of inventory, so little updates may be all you need to tackle. In other areas, there are far more homes for sale, so you may need to do a bit more to make your house stand out.