Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Create a social media post and image for the following information: Buying a vacation home works best when you treat it as both a lifestyle choice and a long-term financial commitment. The smartest approach is to define how you’ll use it, build a full cost budget, and then buy in a location that matches both your travel habits and your management capacity. [zillow](https://www.zillow.com/learn/5-steps-buying-vacation-home/)

## What to decide first

Start by deciding whether the home is mainly for personal use, occasional family getaways, or short-term rental income. That choice affects everything from financing to insurance to how much maintenance you should expect. Also, decide how often you’ll actually visit, because a property that looks perfect on paper can become expensive if it’s too hard to get to. [zillow](https://www.zillow.com/learn/5-steps-buying-vacation-home/)

## Budget beyond the price

The purchase price is only part of the cost. You should also plan for down payment, closing costs, property taxes, insurance, HOA dues, utilities, furniture, cleaning, landscaping, repairs, and any property management fees. Lenders may approve you for more than you should comfortably spend, so it helps to create your own monthly budget first and include the cost of your primary home as well. [zillow](https://www.zillow.com/learn/5-steps-buying-vacation-home/)

## Location matters most

For vacation homes, location is often more important than square footage. Think about climate, seasonality, drive time, or flight cost, nearby activities, rental demand, and local risks like hurricanes, flooding, or wildfire exposure. If you plan to rent the home, local zoning rules and HOA restrictions can make or break the deal. [zillow](https://www.zillow.com/learn/5-steps-buying-vacation-home/)

## Financing and taxes

Vacation homes are usually treated differently from primary residences, so that financing can be stricter and tax treatment can vary depending on how you use the property. A preapproval from a lender before you shop can strengthen your offer and help you understand the real monthly payment before you get attached to a property. If you want rental income, talk to a lender and tax professional early so you understand how use, income, and deductions interact. [zillow](https://www.zillow.com/learn/5-steps-buying-vacation-home/)

## Property type and upkeep

Choose a home type that fits your maintenance tolerance. A condo may be easier to manage, while a house on a beach, lake, or mountain lot may offer more privacy but bring more upkeep, storm prep, and repair costs. If you’ll be absent much of the year, consider security systems, local contacts, and whether there’s nearby storage for items you don’t want exposed to guests if you rent it out. [extraspace](https://www.extraspace.com/blog/moving/consider-before-you-buy-a-vacation-home/)

## Buying process

A practical buying process looks like this:

1. Define your budget and usage goals. [zillow](https://www.zillow.com/learn/5-steps-buying-vacation-home/)

2. Get preapproved by a lender. [staging.lendingtree](https://www.staging.lendingtree.com/home/mortgage/mortgage-for-vacation-home/)

3. Work with a local agent who knows vacation markets and rental rules. [realestate.usnews](https://realestate.usnews.com/real-estate/articles/things-to-consider-before-buying-a-vacation-home)

4. Compare properties using total ownership cost, not just list price. [extraspace](https://www.extraspace.com/blog/moving/consider-before-you-buy-a-vacation-home/)

5. Review inspection, insurance, and HOA details carefully before closing. [zillow](https://www.zillow.com/learn/5-steps-buying-vacation-home/)

## Questions to ask

Before making an offer, ask:

– How often will we really use this home?

– Can we afford it if rental income is lower than expected?

– Who will maintain it when we’re away?

– Are short-term rentals allowed?

– Is the property easy enough to reach for weekends or holidays?

– What are the full carrying costs over a year? [zillow](https://www.zillow.com/learn/5-steps-buying-vacation-home/)

A good vacation home should feel like a retreat, not a second source of stress. The best purchases are usually the ones that still make sense even if plans, markets, or rental demand change. [realestate.usnews](https://realestate.usnews.com/real-estate/articles/things-to-consider-before-buying-a-vacation-home)

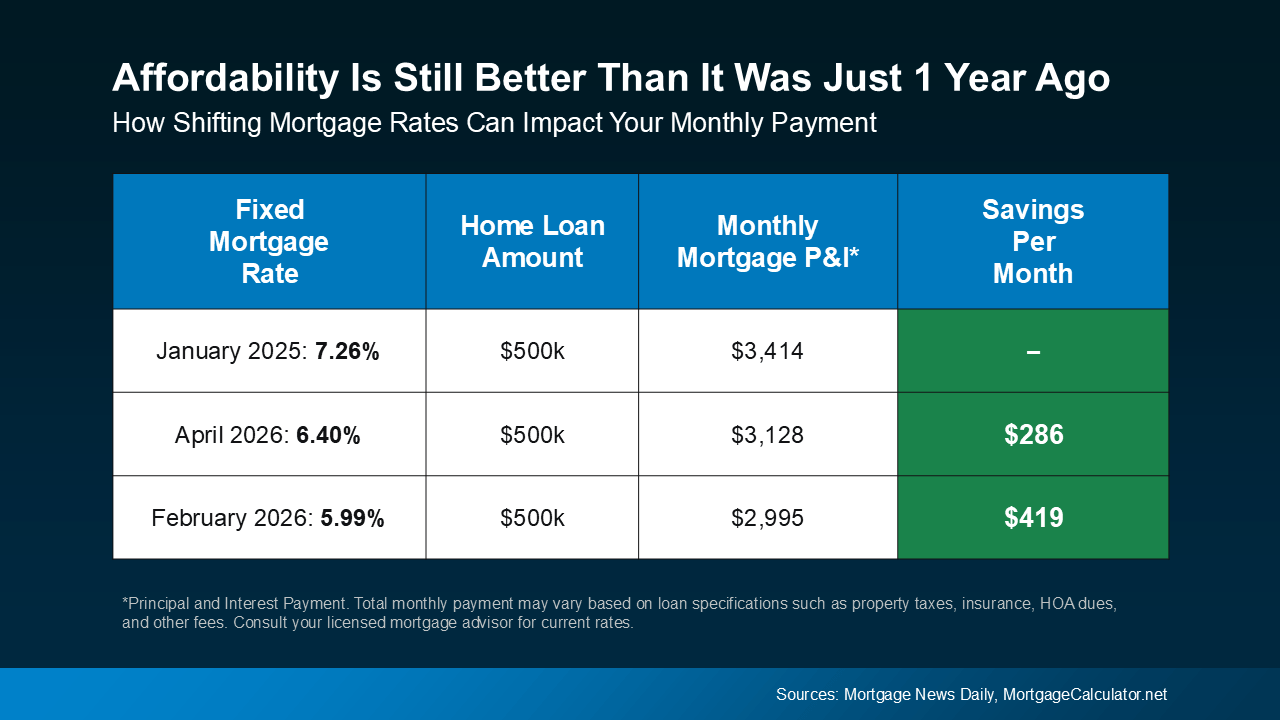

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

So, What Can You Do About It?

So, What Can You Do About It?